By David Schmidt

The global market for alternative data is anticipated to reach $143.31 billion by 2030. That’s substantial to say the least, and the U.S. dominates two-thirds of this market. Over the past year, there have been an escalating number of data providers incorporating novel data procurement and extraction methods, which lends credence to this projection.

This wave has been building for some time. A friend and longtime colleague of mine in the credit space, Rich Ferrera, and I have been researching how the business credit information space is likely to evolve, and may even be disrupted, by modern digital technology. Rich is of the opinion that digital technologies, championed in the Fintech lending and wealth management arenas, are being used to obtain traditional credit risk data and can be used in a more widespread way to improve the data quality in the existing data acquisition processes of the traditional credit information providers.

According to Rich, Jim Swift, while at Cortera, started talking about “alternative data” almost ten years before (D&B) picked the idea up. In 2016, while at D&B, Rich, as Senior Leader of Global Data Assets, and Saleem Khan, Global Leader of Content Innovation, jointly authored an article titled Social Media & Credit Decisioning: Analysis by a leading trade credit services provider. After publishing this article, Rich found that alternative data, such as social media sentiment data and influencer scores, didn’t live up to its expected value and were difficult to implement within existing credit reporting reports and scores. Concurrent with these subsequent discoveries, Rich began to observe new and more modern Fintech technology being used to collect alternative data from more traditional sources of credit data, such as banking history data by OnDeck.

Another example of this is Kabbage, one of the early fintech small business lenders that rose out of the ashes of the Great Recession of 2008 only to be acquired by American Express in 2020. With its initial launch Kabbage did not rely on commercial credit reports to make online lending decisions, which were typically completed in 20 minutes or less. Instead, like many of their competitors, they began using alternate methods to collect traditional credit data, including permissio ]]]]ned access to the borrower’s bank accounts, in order to provide the fuel for their decision engine.

Rich and I are of the opinion that despite the potential benefits new data sources and types bring to the marketplace, verified foundational and firmographic data about a commercial credit seeker, combined with its payment and bank history plus any negative filings, remain the most important data elements to access credit risk. These new ways to collect traditional credit data are in itself a new form of alternative data that warrants close observations because, as we all know, the current state of the industry is long overdue for disruption.

The Current State of Affairs

We believe disruption is overdue because traditional credit information providers are far from perfect and can frustrate their customers by not delivering everything they want. The weaknesses with the B2B distribution channels of D&B, Experian, Equifax and CreditSafe are that they are often slow to update their records, rely on outdated information, and can be expensive. Additionally, they often rely on manual data entry and outdated methods of verification, which can lead to errors and inaccuracies. Furthermore, their products are often tailored towards large enterprises, leaving small and medium-sized businesses without access to the same level of detail.

By utilizing open data, third-party verified data, and self-reported data, businesses can access more timely and accurate information than the bureaus provide, which can help them make better decisions. These alternative data sources may disrupt the commercial credit reporting industry by providing credit grantors with access to more accurate and up-to-date information about the creditworthiness of customers and potential clients. By relying on open data sources, businesses can access financial and non-financial data such as company registration information, accounts receivable data, and other public records. Third-party verified data can supplement open data sources with additional data points such as payment history, financial health, and credit risk scores. Finally, self-reported data from the businesses themselves can provide more detailed insights into the financial health and risk profile of their customers.

Here are some of the problems with the current market for business insights:

- No agency or other business data provider can keep up with the Internet, and now the Cloud, regarding data freshness or completeness of self-reported data

- When agency data is out of sync with self-reported open data available on the Internet, users doubt the veracity of the traditional data (non-open data such as trade payments or scores) even if the competitive data is also wrong

- Traditional big data electronic collection methods often result in too much data on some credit seekers and not enough on many other credit seekers

- Users are frustrated by thin records (business files with minimal information) and price increases for business data – this frustration is expected to grow as data controls prevent the collection of some data (e.g., the EU GDPR and state laws such as California’s CCPA), especially when related to small businesses

- Credit seekers get frustrated when they are denied credit based on incorrect or missing information

- The agencies, to compensate, try to sell products to the business credit seeker to have them update or input additional data to their own reports and this is often unsuccessful because of data controls and restrictions on accessing data – in some circumstances, credit seekers have been deceived when purchasing these products (the FTC claims Dun & Bradstreet deceived small businesses about services and pricing)

Not to pick on the credit bureaus and other traditional business data sources, but the business information industry operates in a very challenging market. In the USA, there are currently nearly 34 million businesses. According to the US Chamber of Commerce, there are 33.2 million small businesses (50 employees or less) in this country – that’s a 75 percent increase over the past 25 years. Of those small firms, 27.1 million have no employees and Census Bureau statistics going back decades consistently indicate only half of all small businesses make it to their 5th anniversary. Moreover, since the onset of Covid, 5.4 million new businesses have been launched. In contrast, large businesses and public businesses, on which it is much easier to develop information, only total in the tens of thousands. This is obviously a very dynamic marketplace to try and track, and the traditional information providers have clearly done yeoman work in developing their products.

The Opportunity for Alternative Data

The current state of affairs cries out for better data solutions. This does not mean traditional business information no longer has any use. Instead, it is an opportunity for alternative data to fill in many of the gaps in the current business data eco-system. As Kevin King, VP of Credit Strategy at LexisNexis Risk Solutions, observes, "There's an opportunity to pull in more relevant information to make better lending decisions, and we're just really at the start of that era." Before we delve into that, we first need to define the different types of alternative data in more detail:

Self-Reported Data: Most businesses have a web-presence, which is a good source of self-reported data. Today, much directory data is also self-reported. Take Yelp for example. A business owner looks up his own business listing online, claims that listing, and then fills in the missing details (maybe correcting some of the details already there). The primary issue with self-reported data involves verification. A credit executive does not accept the information submitted on a credit application without first verifying it. The best sources of self-reported data will also provide verification.

Permissioned Data: Also know as consent data, this is a situation where the business owner allows another service provider or vendor to access the business’ account data. The most common scenario involves bank account information, which the business grants permission to a third party to access. Online lenders like to see the last three to six months bank statements from an applicant and the easiest, fastest, and best way to get at that information for all involved is with the applicant’s permission. upSWOT, an embedded finance and business management platform that enables SMBs to connect their accounting, ERP, payroll, eCommerce, marketing, CRM, and other applications to their bank, reports that roughly a third of SMBs are willing to provide financial institutions with continuous opt-in access to their company bank records. It should not take a giant leap to add similar access to payment records collected and shared within industry trade credit associations, of which there are more than 1,000 in the U.S.

Open-Source Data: Thanks to the Internet there is now a wealth of public information on businesses that is readily available online. There are several different sources of this business information. News services, industry sources, and the government provide us with a wealth of information on individual businesses. Sentiment data also falls under this heading. Customer ratings on Yelp, Doordash, Google, and other social media archives can tell you a lot about individual businesses. Taking it a step further, Middesk is helping organizations easily extract meaningful data from various media to better understand customers, monitor competitors, and visualize market intelligence.

Internal Data: Different types of alternative data each have their own advantages and benefits. When access to this external data is embedded in other digital financial applications such as ERP, CRM, or credit and collection software systems, its value can be multiplied. Alternative data extends beyond standard financial data to provide context for understanding company performance, customers, and market dynamics.

Where Are We Headed?

There is a huge macroeconomic upside for the insights derived from alternative data assets, and they are expected to spur growth worldwide and across practically every industry sector. Artificial Intelligence (AI) and Machine Learning (ML) are not only going to make the job of gleaning insights easier from the volumes of data available but are also going to open up new opportunities for leveraging alternative data insights.

Tools such as Google Trends are already being used to this end. In this case, by auditors to confirm financial reports. Researchers have discovered that high-demand retail products typically spawn the most searches, so any misalignment of revenue growth and search volume brings into question a company’s financial reporting (WSJ, One Way to Spot Red Flags in Companies’ Financials, June 6, 2024).

While public data will always be valuable despite any quality issues because it is easier to obtain, the holy grail of actionable insights lays with data that is only available with permission. "We haven't seen a ton of activity in our engagements on permissioned or consent-based data. I certainly think that's the ultimate direction a lot of people will try and get to, and I think we'll get to that point faster on commercial lending than in consumer lending," says King.

Part of the challenge is getting the right data to support any decision process. There is so much data available that gathering everything with relevance could prove to be a fool’s errand. In addition, data from around the world comes in a multitude of forms and types. What’s required is a process mentality. "The problem is much broader than just access to data; it's a workflow problem, and many customers have very manual-intensive processes,” states Michael Ramsbacher, Chief Product Officer at Trulioo, a provider of an identity and business verification platform that can hook their clients into 195 different countries.

The issue for users then is to not just access the data but also have the right tools and processes to generate insights. "Banks and financial institutions are using consent data from customer accounts in different ways, so how we are delivering it is important. For one of our use cases, we deliver an administrative panel where banks are able to access the data in a formalized way.

They are able to see information on their customer's accounts in other banks, financial metrics, and actionable insights designed to power sales efficiency and make bankers more proactive and supportive," claims Pavlo Martinovych, Head of Product at Upswot, which provides banks with an embedded finance and business management platform for their commercial customers.

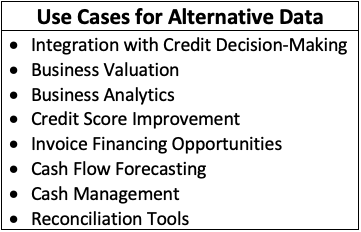

For the lender or trade credit grantor, alternative data offers the hope of better decisions, faster decisions, and even more decisions with regard to situations where the lack of data previously precluded a credit approval. As the accompanying table illustrates, alternative data will also benefit financial managers across a variety of scenarios.

The challenge is to formulate and integrate alternative data into existing processes. That will require reevaluating existing processes, often redesigning those processes as well as developing new processes to facilitate new applications. To a large extent this is going on.

Over the past year, we have identified over one hundred vendors that are working with or developing alternative data, leaving no doubt that this is an emerging market. Some of these vendors are developing commercial credit risk solutions while others are focused on supply chain risks. Still others are working to enhance Know Your Customer (KYC) or other types of compliance scenarios and another groups is dedicated to providing more targeted marketing insights. Within each of these areas, we see a myriad of approaches being tried, but the common goal is more comprehensive data insights to drive better decisions.

++++++

Rich Ferrera is a lifetime NACM Certified Credit Executive and had a 40 plus year career with Dun & Bradstreet in leadership positions involving data and product implementation. Rich is currently consulting with commercial credit information providers and helping investors, lenders and consultants better understand the commercial data management space.

David Schmidt began his business credit career in 1976 with Dun & Bradstreet before moving into corporate credit management. In 1994 he founded A2 Resources, a management consultancy focusing on receivables, credit and collection automation. In 1998 he co-authored "Power Collecting: Automation for Effective Asset Management" (John Wiley & Sons), the seminal text on receivables automation, served almost 20 years as Editor with Credit Today, and has been published extensively in periodicals including Business Credit, Business Finance, and Collection Advisor magazines. In addition, David has been the lead analyst on many research reports covering AR automation and other order-to-cash technologies.

Recent Comments